The NDIS is a growing industry that is benefiting from a newly developed funding model that gives participants choice and control over how they manage their supports.

The reality is that the industry needs 10’s of thousands of workers in order to supply the supports that participants need. Importantly, the variety of services needed under the NDIS is diverse and highly personal.

For individuals, there is a growing opportunity to establish themselves as a self-employed professional in the industry and grow a business that helps individual participants in their day-to-day lives.

Taking the first step to self-employment can be daunting, so we have put together a 7-step guide to walk you through how to get setup quickly and easily in the NDIS. Our hope is that it helps more people join the industry and make a difference in people’s daily lives by providing the services participants are looking for.

1. Becoming a sole trader

Becoming a sole trader with your own business is as simple as making the decision that this is the direction you want to take. Starting out as a sole trader is the most common course people take and sole traders represent the largest number of new businesses for a reason, it is quick, easy and inexpensive to setup.

Depending on your circumstances you may want to consider setting up under a different structure like a company, partnership or trust. There are a range of different business structures available and each have their own pro’s and con’s, make sure you read up on the differences and get professional advice if you need it.

This article is going to focus on becoming a sole trader because one of the biggest blockers for people looking to start out is taking that first step. If you go and add layer and layer of complexity before you have even started, you may end up chasing your tail forever.

So, what’s so great about being a sole trader?

Becoming self-employed as a sole trader is the most accessible gateway to take control of your working life. ‘Being your own boss’ is becoming a cliché as self-employment grows in popularity, but it’s more than that. In a world where we are becoming more and more time poor and being pulled in a million directions we may not necessarily agree with, self-employment offers the ability to do it your way. It’s being able to choose the clients you want to work with, charging the rate you know you’re worth, balancing work with all the other commitments life throws at you.

Now there are a few essentials you need to do to get the ball rolling.

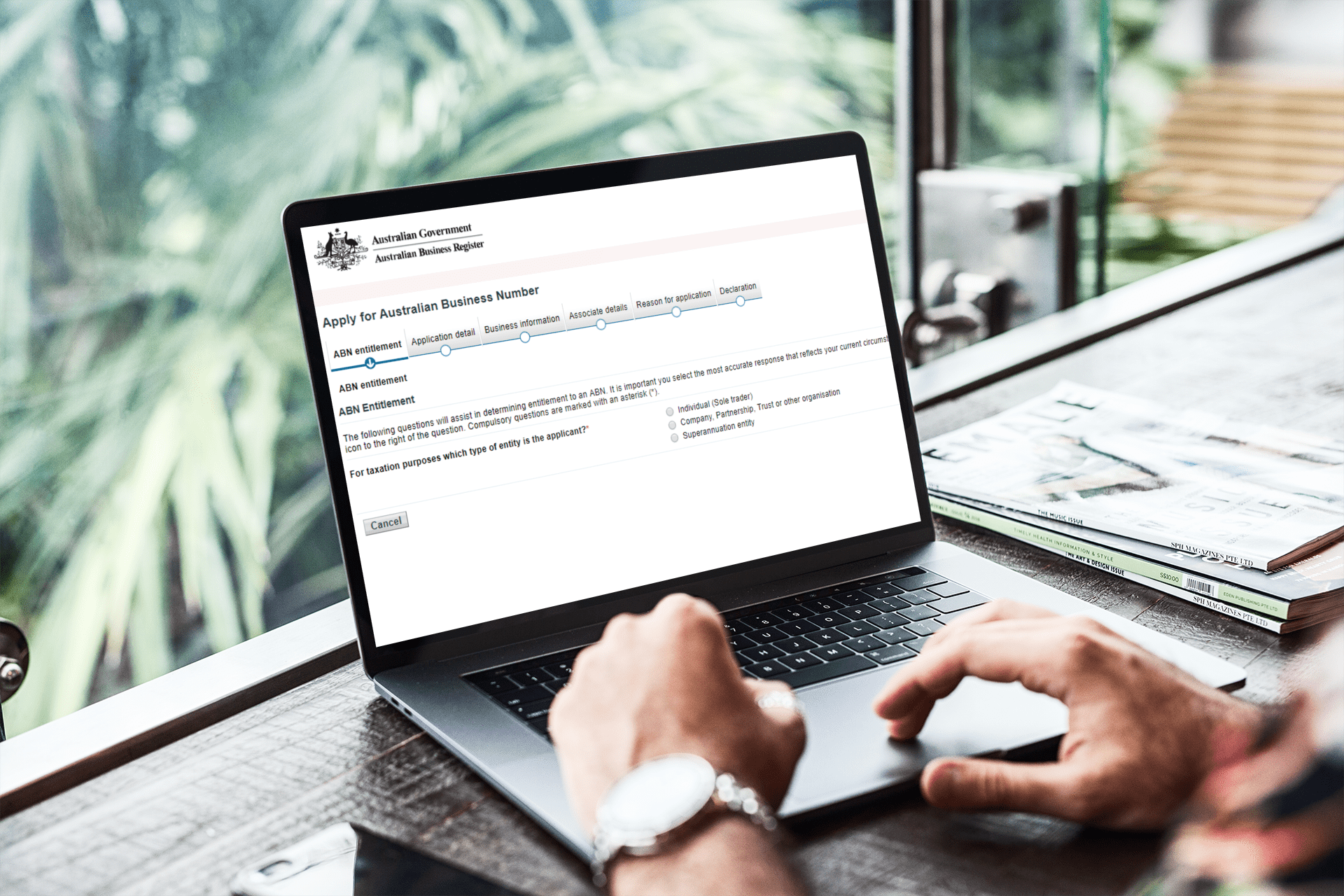

2. Registering an ABN

First things first, you are going to need an Australian Business Number or ABN if you want to run a business in Australia. An ABN is an 11-digit number issued by the Australian Business Register (ABR) as a way of tracking all businesses in Australia, P.S it’s a legal requirement.

Applying for an ABN as a sole trader is completely free, watch out for the paid ads that want to charge you for it if you’re googling it. The process only takes 10-15 minutes and asks you for some basic info to get setup.

It’s a good idea to get some help from someone in the know to help walk you through it as some of the questions can be a little confusing.

In most cases you will get the ABN as soon as you have submitted your application, congratulations you are officially registered as an Australian business.

3. Business Bank Account

A business bank account is going to be the lynchpin to your financial success as a self-employed business owner and I couldn’t recommend it highly enough. Here’s why:

As a self-employed business owner, you are going to need to be able to report on all your business income and all your business expenses. Each quarter or year this info needs to be put together and reported to your accountant and on to the tax office. Believe me, if you have this mixed in with your personal accounts you are setting yourself up for a lot of tedious and annoying paperwork.

Having a separate business bank account for your business is a track way to simplify tracking and managing all the in’s and outs of the business.

As your business grows, you are also going to need to account for financial commitments within the business or building up profit in the business. A huge advantage of having a separate business bank account is that you can easily separate your income and the businesses income. While you may want to consider them the same thing, having them separated can be a powerful financial planning and saving vehicle.

4. Invoicing & Quoting

Once you get to the point of sending out your first quote or better yet, invoice for your services, is when you can start to have a lot of fun. But don’t be fooled, there is an art to invoicing and quoting and keeping up with best practice will help you stay professional, organised and on-track to getting paid on time.

When you’re sending out quotes it means that you are putting together a pricing document for a potential client to review the services you’re offering and the associated cost. By its very nature, a quote means you haven’t won the business yet. Best practice is all about showing up professionally as a reliable and trustworthy option.

When it comes time to send out your invoice there are a range of tips and tricks that will help you leave your client with a great experience and minimise the time to payment.

• Be thorough and specific: Itemise all the services provided on your invoice so the client can see exactly what they are paying for. This can save a lot of back and forth if people have forgotten certain aspects of the service.

• Leave a message: Giving the client some positive feedback on your experiences can be a great way to build a long-term relationship.

• Be timely: Don’t wait to send the invoice through, the quicker you send it through to your client the more likely it is to get paid on time.

• Put in the detail: This is especially important for operating in the NDIS where you may need to spell out the specifics of the work in order to claim through the NDIA. Things like the participant name, participant number, item codes should be clearly visible on the invoice. If you are unsure of the codes, you can check with the participant, plan manager, registered provider or the NDIA to get clarification.

5. Managing Receipts

Managing your expenses and keeping track of your receipts once again comes down to being on top of your financial obligations as a business. You see, business expenses are often tax deductible and are important to report to ensure you don’t over pay on your tax. In order to correctly claim for the business expenses, you need to have proof of the expense in the form of a tax receipt. The tax office will take your word for it but regularly conduct audits to check you are keeping adequate financial records.

The typical scenario is the shoe box or glove compartment full of receipts that are in a complete state of chaos. Thankfully, technology has advanced that the tax office will accept electronic copies of your receipts. This opens the door to a whole new simplified way of keeping and tracking your expenses.

Using technology to help keep your receipts organised will help you in several ways:

• Keep up to date with your expenses: There is no reason why you need to be in the dark, by tracking your receipts you will be able to get current data and reports showing how much you are spending on your business expenses.

• Simplify reporting: Being able to report the details of your expenses to either your accountant or the tax office will save you a bunch of time and money in the long run.

• Don’t lose receipts: It’s amazing how small receipts are and how quickly the ink fades to nothing. Storing a photo of a receipt electronically ensures its longevity and stops them getting lost in the day-to-day.

![]()

6. Insurance

When you are running a business as a sole trader, it’s important that you take steps to insure yourself against any unforeseen incidents. The reality is that accidents happen, and insurance is a critical part of any business.

There are a range of insurances available and you should speak with a professional to get the right advice for your circumstances. This can be particularly specific to the work you are doing, for example if you help participants take their medication, that specific task may not generally be covered under an insurance policy.

Here are a few of the key insurances and what they generally provide cover for:

• Public Liability: is insurance that covers you for damage to a third-party in the course of the work you do. That may include the participant themselves or someone else from the community.

• Personal Accident & Sickness: This insurance covers your own financial well-being in the event that you are sick or injured and can no longer work.

• Professional Indemnity: is insurance that covers you for advice and instructions you may be giving and can include participants or other providers.

7. Registrations & Licenses

The type of registrations and licenses required will vary greatly depending on the type of work you are going to be providing.

• Qualifications: Having current and up to date qualifications such as police checks and working with children checks are commonplace in the NDIS industry.

• NDIS Registration: Going through the NDIA registration process to become a registered provider is an obvious decision a business makes early on. The reality is that being a registered provider is not a requirement in many circumstances to work in the NDIS. There are many pro’s and con’s that come along with registration and the decision will depend on your circumstances. For many sole traders starting out in the industry the cost and documentation required to reach and maintain registration is very high. It is common for individuals to start out un-registered in the NDIS and build their business up to a point that they can become registered.

• General Registrations: It’s important to check NDIA, government and local council requirements for the work you are doing. For example, if you are using space in a council park you may need to book that spot.

Congratulations on taking some time to explore the opportunity the NDIS provides for self-employed individuals to make the most of their unique talents. The industry is thriving and growing by the day and is in desperate need of highly motivated, professional and caring individuals to provide such a wide range of services.

Self-employment offers so many opportunities for people to control their working lives and balance all their commitments. Nobody said self-employment was easy, but the benefits that flow into all aspects of life are un-rivalled.

We wish you all the best in your journey.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}